import pandas as pd

import plotnine as p9

from plotnine import *

from plotnine.data import *

import numpy as npTime Series Forecasting with Python: Method 1

Loading packages

Read data

airpassenger = pd.read_csv('AirPassengers.csv')

airpassenger['Month']= pd.to_datetime(airpassenger['Month'])Visualise data

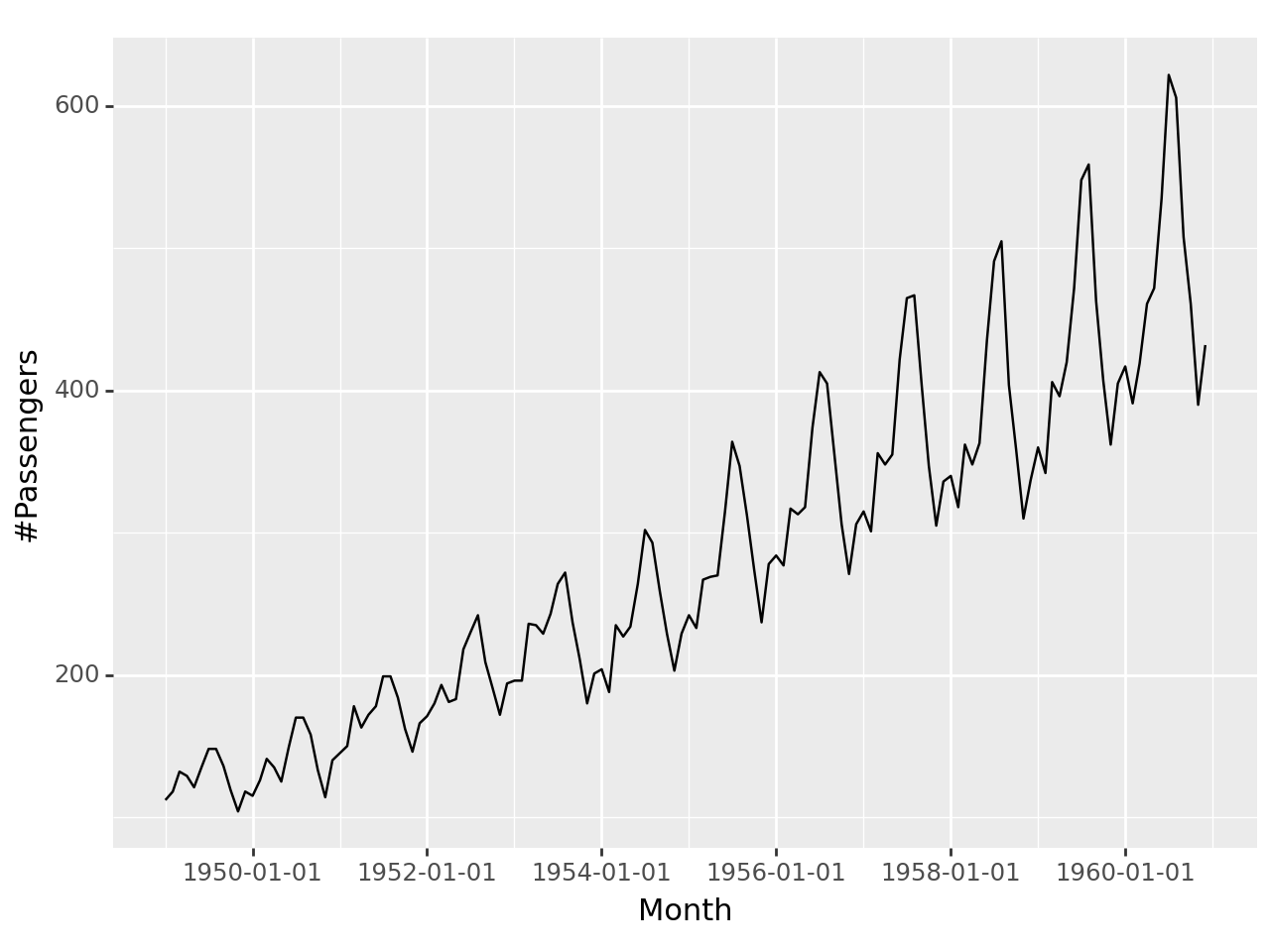

ggplot(airpassenger, aes(x='Month', y='#Passengers'))+geom_line()

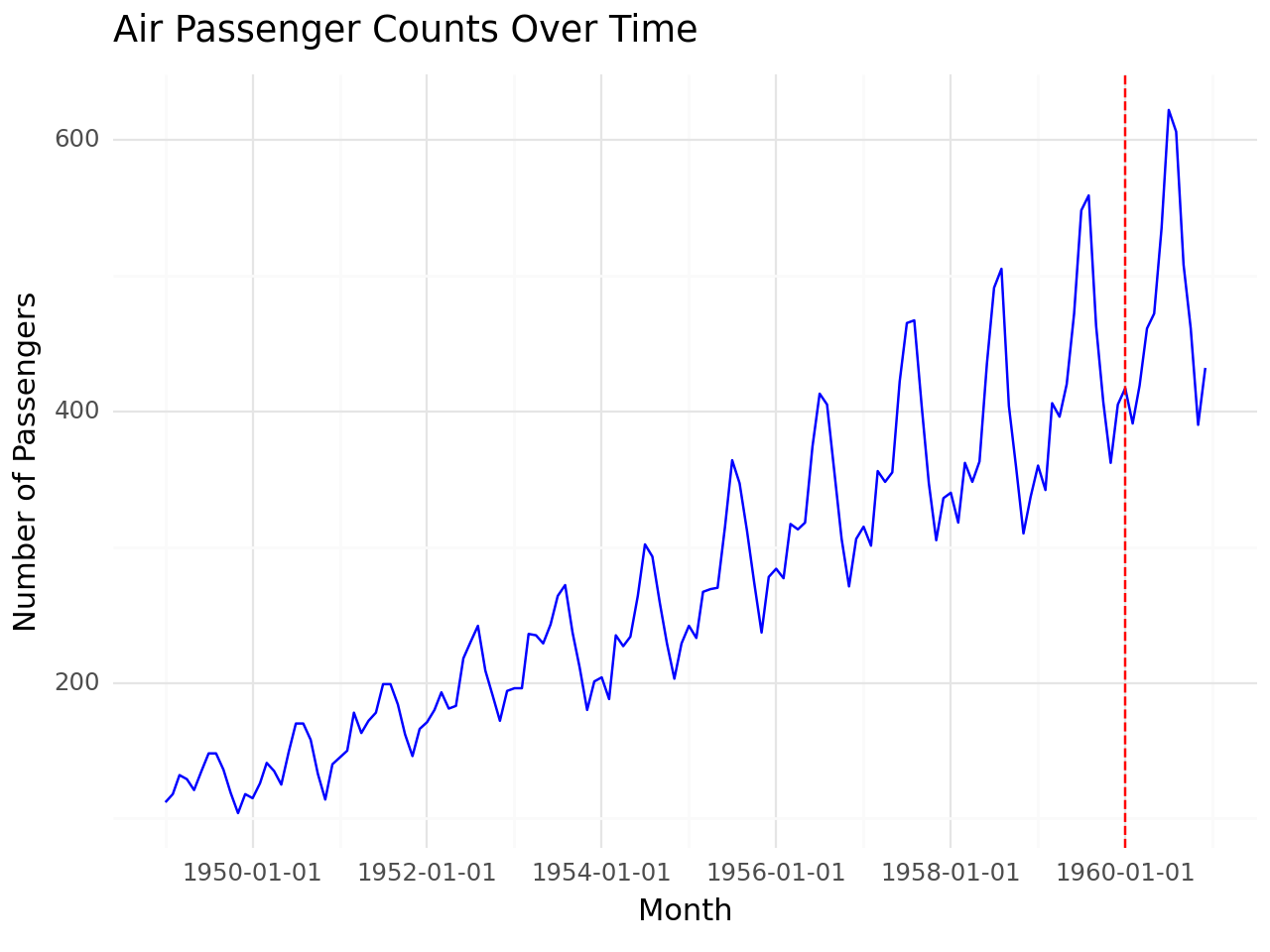

Training set vs Test set

# Define training and test separation point

split_date = '1960-01'

# Visualize data

g = (

ggplot(airpassenger, aes(x='Month', y='#Passengers')) +

geom_line(color='blue') +

geom_vline(xintercept=pd.to_datetime(split_date), linetype='dashed', color='red') +

labs(

title='Air Passenger Counts Over Time',

x='Month',

y='Number of Passengers'

) +

theme_minimal()

)

# Print plot

print(g)

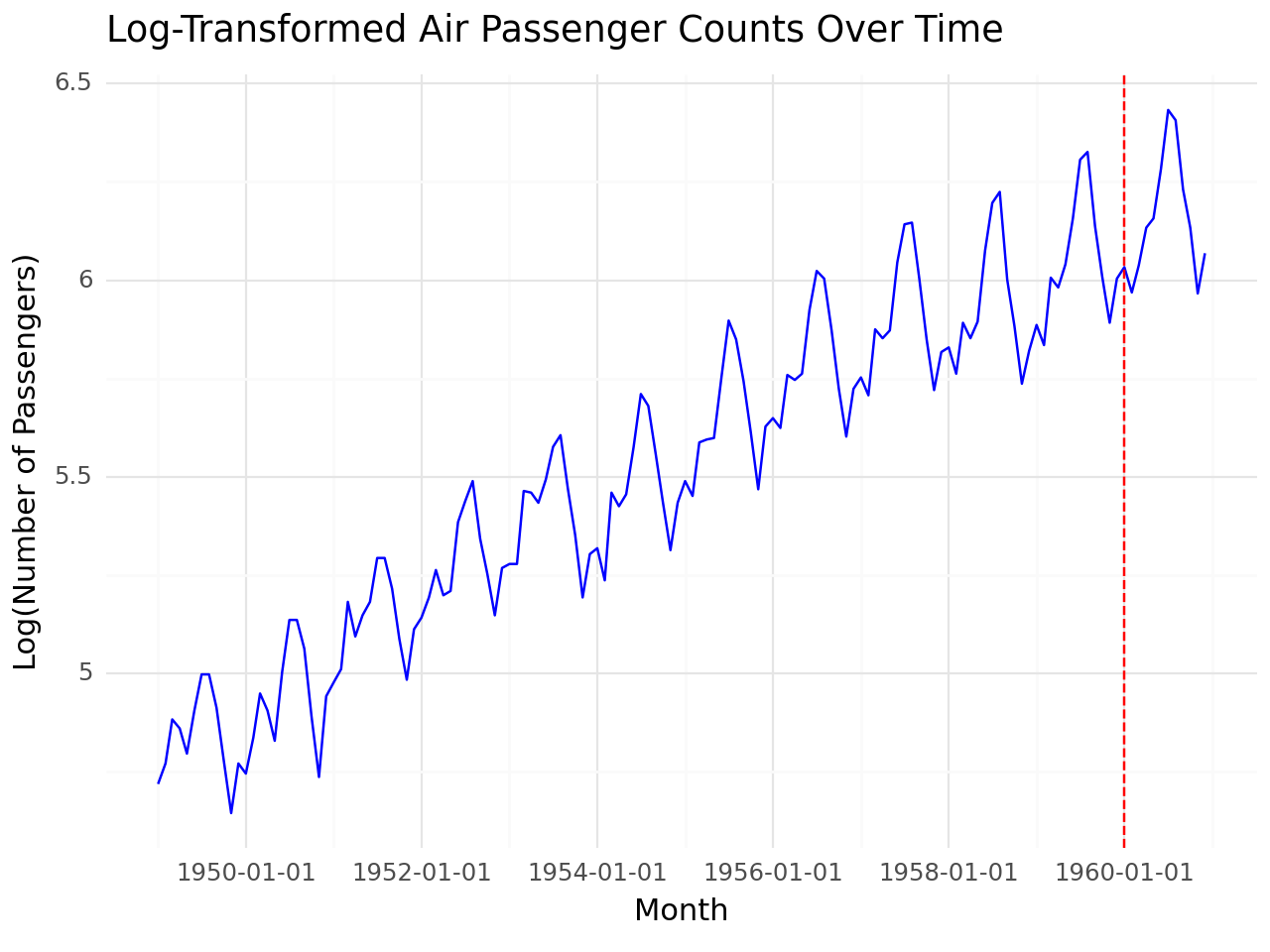

Apply log transformation

airpassenger['Log_Passengers'] = np.log(airpassenger['#Passengers'])

# Define training and test separation point

split_date = '1960-01-01'

# Visualize data

g = (

ggplot(airpassenger, aes(x='Month', y='Log_Passengers')) +

geom_line(color='blue') +

geom_vline(xintercept=pd.to_datetime(split_date), linetype='dashed', color='red') +

labs(

title='Log-Transformed Air Passenger Counts Over Time',

x='Month',

y='Log(Number of Passengers)'

) +

theme_minimal()

)

# Print plot

print(g)

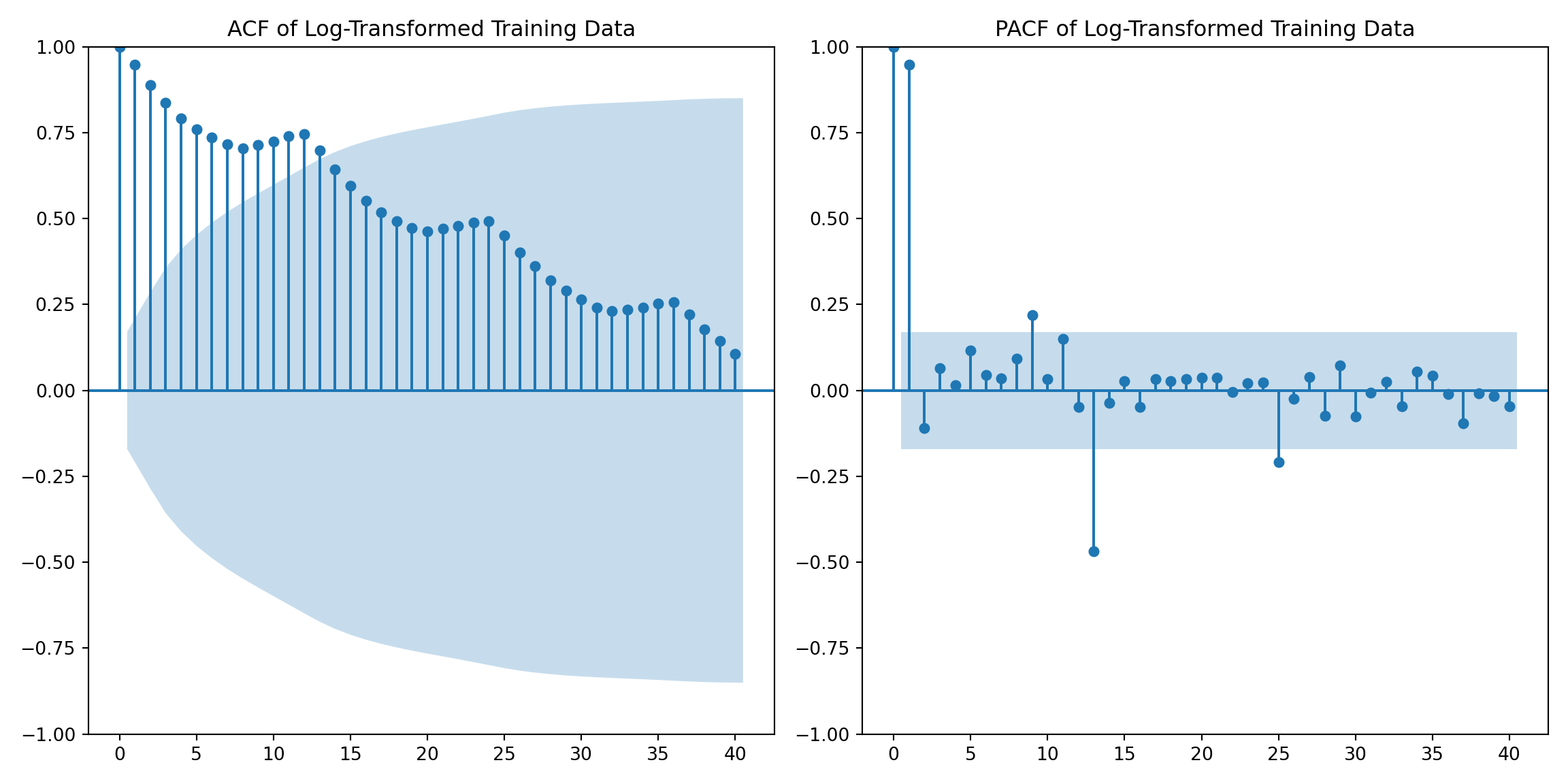

Set training data set and test dataset

training_data = airpassenger[airpassenger['Month'] < pd.to_datetime(split_date)]

test_data = airpassenger[airpassenger['Month'] >= pd.to_datetime(split_date)]Plot ACF and PACF for training data

import matplotlib.pyplot as plt

from statsmodels.graphics.tsaplots import plot_acf, plot_pacf

plt.figure(figsize=(12, 6))

plt.subplot(1, 2, 1)

plot_acf(training_data['Log_Passengers'], lags=40, ax=plt.gca())

plt.title('ACF of Log-Transformed Training Data')

plt.subplot(1, 2, 2)

plot_pacf(training_data['Log_Passengers'], lags=40, ax=plt.gca(), method='ywm')

plt.title('PACF of Log-Transformed Training Data')

plt.tight_layout()

plt.show()

Apply First-Order Seasonal Difference and Obtain ACF and PACF

airpassenger['LogSeasonal_Diff'] = airpassenger['Log_Passengers'] - airpassenger['Log_Passengers'].shift(12)

airpassenger.head(14)| Month | #Passengers | Log_Passengers | LogSeasonal_Diff | |

|---|---|---|---|---|

| 0 | 1949-01-01 | 112 | 4.718499 | NaN |

| 1 | 1949-02-01 | 118 | 4.770685 | NaN |

| 2 | 1949-03-01 | 132 | 4.882802 | NaN |

| 3 | 1949-04-01 | 129 | 4.859812 | NaN |

| 4 | 1949-05-01 | 121 | 4.795791 | NaN |

| 5 | 1949-06-01 | 135 | 4.905275 | NaN |

| 6 | 1949-07-01 | 148 | 4.997212 | NaN |

| 7 | 1949-08-01 | 148 | 4.997212 | NaN |

| 8 | 1949-09-01 | 136 | 4.912655 | NaN |

| 9 | 1949-10-01 | 119 | 4.779123 | NaN |

| 10 | 1949-11-01 | 104 | 4.644391 | NaN |

| 11 | 1949-12-01 | 118 | 4.770685 | NaN |

| 12 | 1950-01-01 | 115 | 4.744932 | 0.026433 |

| 13 | 1950-02-01 | 126 | 4.836282 | 0.065597 |

airpassenger.tail(12)| Month | #Passengers | Log_Passengers | LogSeasonal_Diff | |

|---|---|---|---|---|

| 132 | 1960-01-01 | 417 | 6.033086 | 0.146982 |

| 133 | 1960-02-01 | 391 | 5.968708 | 0.133897 |

| 134 | 1960-03-01 | 419 | 6.037871 | 0.031518 |

| 135 | 1960-04-01 | 461 | 6.133398 | 0.151984 |

| 136 | 1960-05-01 | 472 | 6.156979 | 0.116724 |

| 137 | 1960-06-01 | 535 | 6.282267 | 0.125288 |

| 138 | 1960-07-01 | 622 | 6.432940 | 0.126665 |

| 139 | 1960-08-01 | 606 | 6.406880 | 0.080731 |

| 140 | 1960-09-01 | 508 | 6.230481 | 0.092754 |

| 141 | 1960-10-01 | 461 | 6.133398 | 0.124585 |

| 142 | 1960-11-01 | 390 | 5.966147 | 0.074503 |

| 143 | 1960-12-01 | 432 | 6.068426 | 0.064539 |

Remove rows with NaN values from the airpassenger DataFrame

airpassenger.dropna(inplace=True)

# Display the cleaned DataFrame

print(airpassenger) Month #Passengers Log_Passengers LogSeasonal_Diff

12 1950-01-01 115 4.744932 0.026433

13 1950-02-01 126 4.836282 0.065597

14 1950-03-01 141 4.948760 0.065958

15 1950-04-01 135 4.905275 0.045462

16 1950-05-01 125 4.828314 0.032523

.. ... ... ... ...

139 1960-08-01 606 6.406880 0.080731

140 1960-09-01 508 6.230481 0.092754

141 1960-10-01 461 6.133398 0.124585

142 1960-11-01 390 5.966147 0.074503

143 1960-12-01 432 6.068426 0.064539

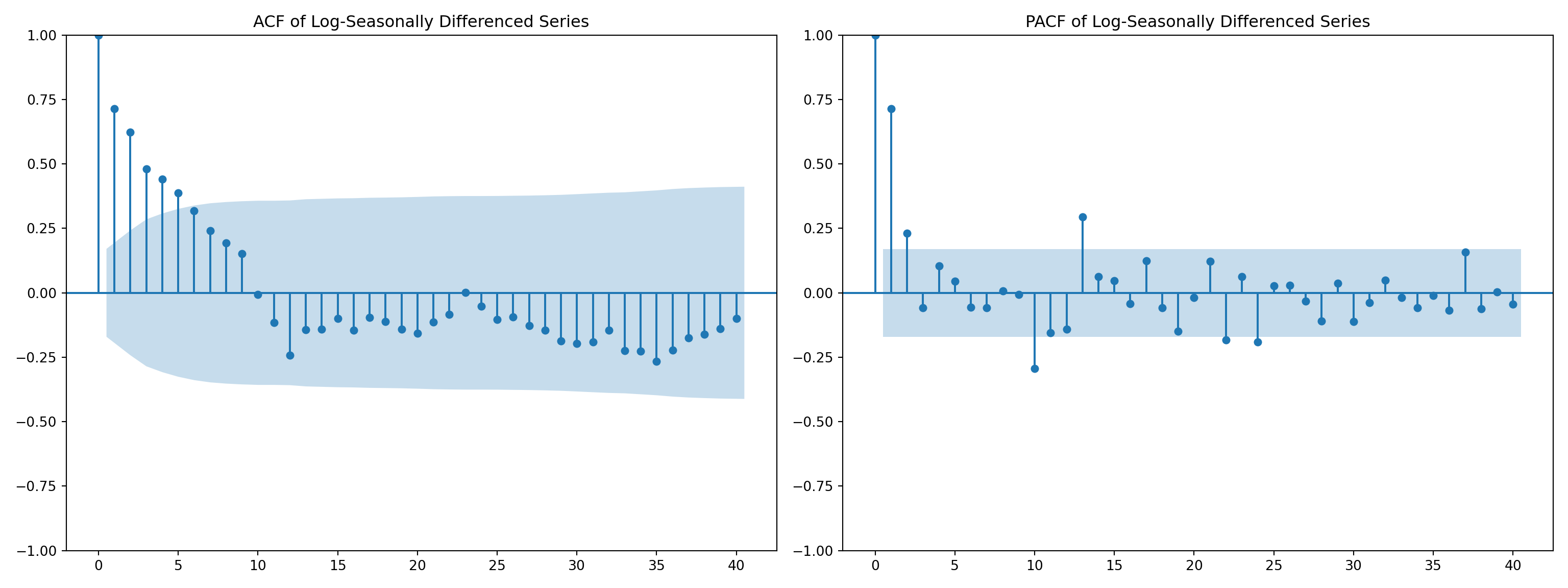

[132 rows x 4 columns]Plot ACF and PACF of the log-seasonally differenced series

fig, axes = plt.subplots(1, 2, figsize=(16, 6))

# ACF plot

plot_acf(airpassenger['LogSeasonal_Diff'], ax=axes[0], lags=40)

axes[0].set_title('ACF of Log-Seasonally Differenced Series')

# PACF plot

plot_pacf(airpassenger['LogSeasonal_Diff'], ax=axes[1], lags=40)

axes[1].set_title('PACF of Log-Seasonally Differenced Series')

plt.tight_layout()

plt.show()

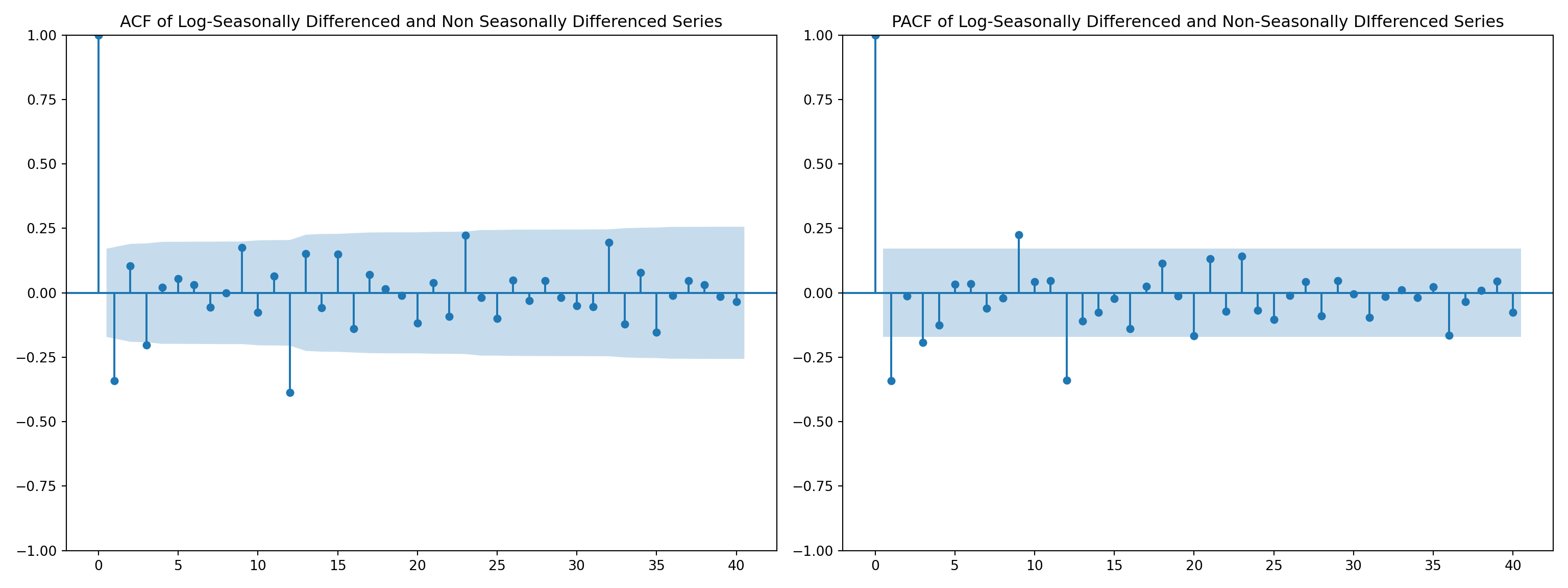

Apply First-Order Differencing

airpassenger['LogSeasonal_Diff.NonSeaDiff'] = airpassenger['LogSeasonal_Diff'] - airpassenger['LogSeasonal_Diff'].shift(1)

airpassenger.head(14)

airpassenger.dropna(inplace=True)fig, axes = plt.subplots(1, 2, figsize=(16, 6))

# ACF plot

plot_acf(airpassenger['LogSeasonal_Diff.NonSeaDiff'], ax=axes[0], lags=40)

axes[0].set_title('ACF of Log-Seasonally Differenced and Non Seasonally Differenced Series')

# PACF plot

plot_pacf(airpassenger['LogSeasonal_Diff.NonSeaDiff'], ax=axes[1], lags=40)

axes[1].set_title('PACF of Log-Seasonally Differenced and Non-Seasonally DIfferenced Series')

plt.tight_layout()

plt.show()

Fit ARIMA(0,1,1)(0,1,1)[12] model

from statsmodels.tsa.arima.model import ARIMA

model = ARIMA(airpassenger['Log_Passengers'], order=(0, 1, 1), seasonal_order=(0, 1, 1, 12))

fitted_model = model.fit()

forecast = fitted_model.forecast(steps=13)

forecastC:\Users\DELL\AppData\Local\Programs\Python\Python312\Lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: An unsupported index was provided and will be ignored when e.g. forecasting.

C:\Users\DELL\AppData\Local\Programs\Python\Python312\Lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: An unsupported index was provided and will be ignored when e.g. forecasting.

C:\Users\DELL\AppData\Local\Programs\Python\Python312\Lib\site-packages\statsmodels\tsa\base\tsa_model.py:473: ValueWarning: An unsupported index was provided and will be ignored when e.g. forecasting.

C:\Users\DELL\AppData\Local\Programs\Python\Python312\Lib\site-packages\statsmodels\tsa\base\tsa_model.py:836: ValueWarning: No supported index is available. Prediction results will be given with an integer index beginning at `start`.

C:\Users\DELL\AppData\Local\Programs\Python\Python312\Lib\site-packages\statsmodels\tsa\base\tsa_model.py:836: FutureWarning: No supported index is available. In the next version, calling this method in a model without a supported index will result in an exception.131 6.110396

132 6.053819

133 6.171650

134 6.199400

135 6.232725

136 6.368919

137 6.507530

138 6.503117

139 6.324834

140 6.209196

141 6.063624

142 6.168173

143 6.206753

Name: predicted_mean, dtype: float64Residual Analysis

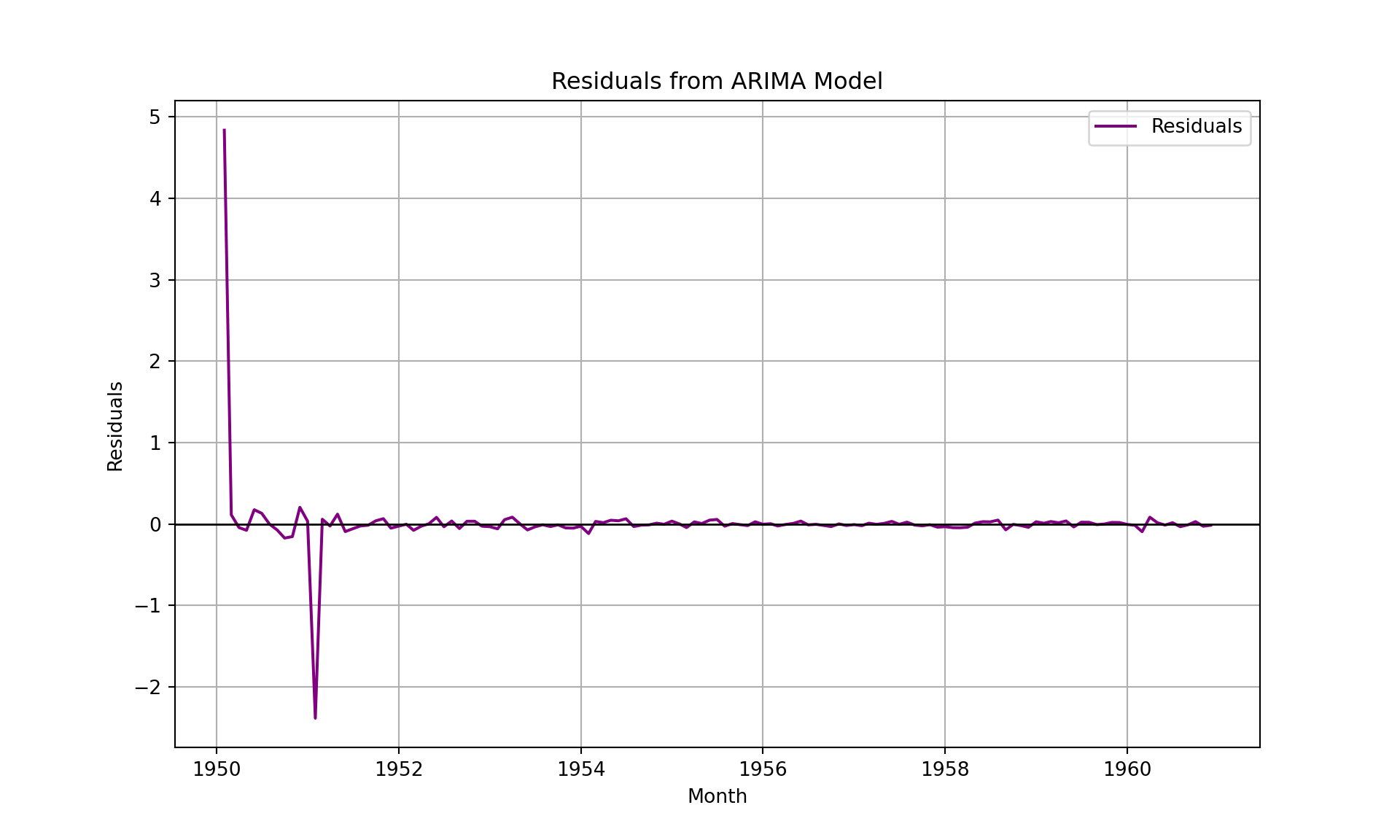

import seaborn as sns

# Compute residuals

train_forecast = fitted_model.fittedvalues

residuals = airpassenger['Log_Passengers'] - train_forecast

# Plot residuals

plt.figure(figsize=(10, 6))

plt.plot(airpassenger['Month'], residuals, label='Residuals', color='purple')

plt.axhline(0, color='black', linewidth=1)

plt.title('Residuals from ARIMA Model')

plt.xlabel('Month')

plt.ylabel('Residuals')

plt.legend()

plt.grid(True)

plt.show()

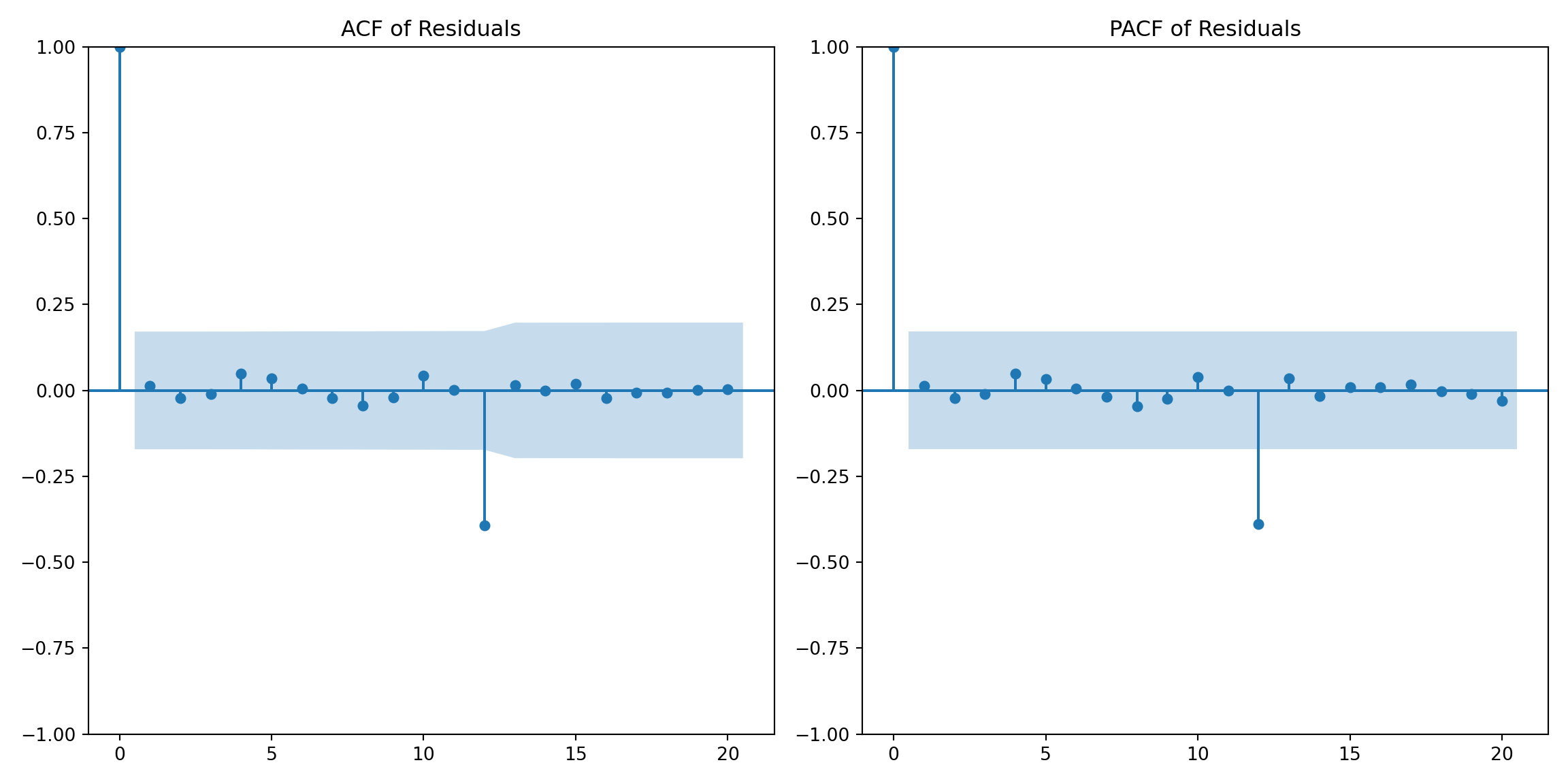

# Plot the ACF and PACF of residuals to check for autocorrelation

plt.figure(figsize=(12, 6))

plt.subplot(1, 2, 1)

plot_acf(residuals, lags=20, ax=plt.gca())

plt.title('ACF of Residuals')

plt.subplot(1, 2, 2)

plot_pacf(residuals, lags=20, ax=plt.gca())

plt.title('PACF of Residuals')

plt.tight_layout()

plt.show()

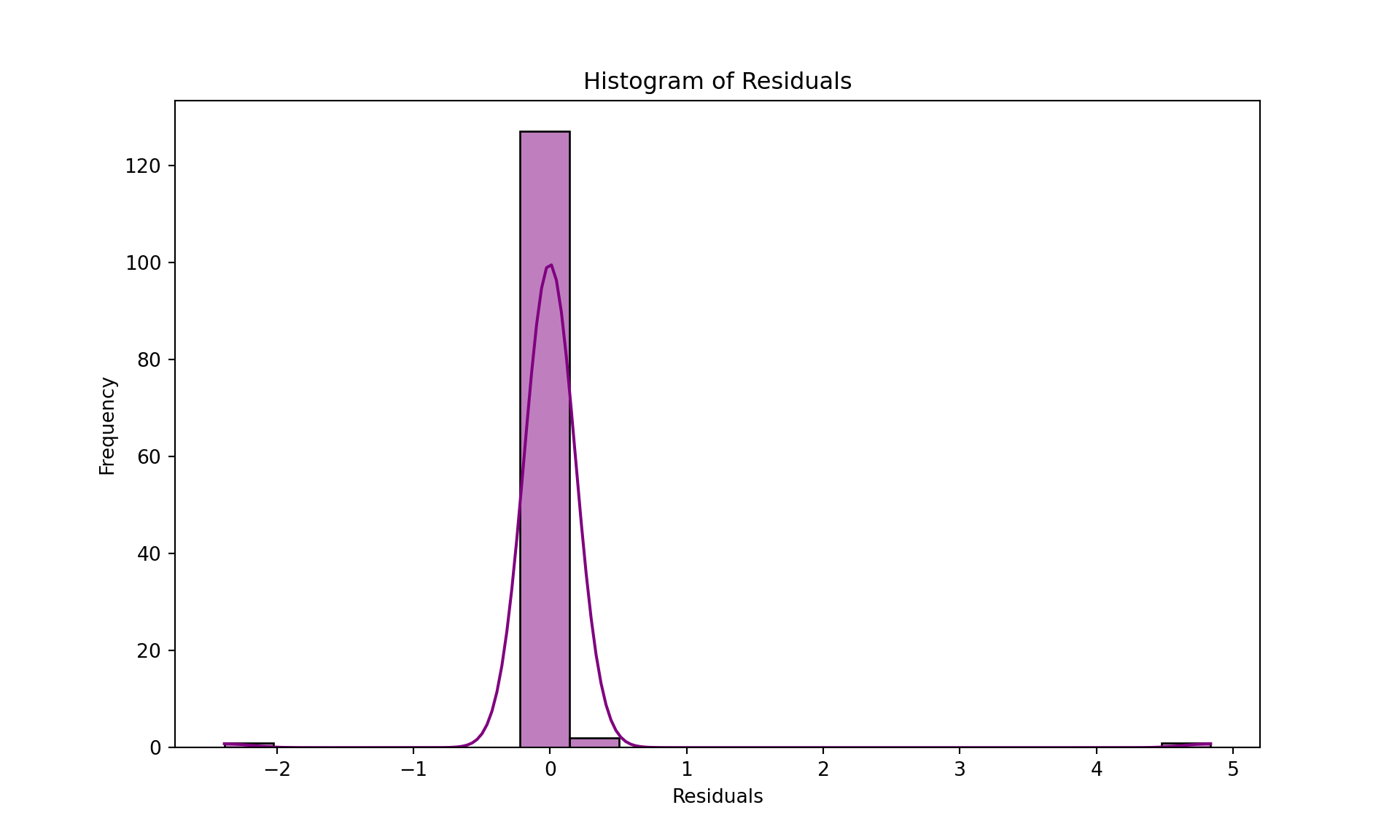

# Histogram of residuals to check for normality

plt.figure(figsize=(10, 6))

sns.histplot(residuals, kde=True, color='purple', bins=20)

plt.title('Histogram of Residuals')

plt.xlabel('Residuals')

plt.ylabel('Frequency')

plt.show()

Back-transform forecasted log values to original scale

forecast_original = np.exp(forecast)

test_data['forecast_log'] = forecast

test_data['forecast_passengers'] = forecast_original

test_dataC:\Users\DELL\AppData\Local\Temp\ipykernel_9236\3410330437.py:2: SettingWithCopyWarning:

A value is trying to be set on a copy of a slice from a DataFrame.

Try using .loc[row_indexer,col_indexer] = value instead

See the caveats in the documentation: https://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#returning-a-view-versus-a-copy

C:\Users\DELL\AppData\Local\Temp\ipykernel_9236\3410330437.py:3: SettingWithCopyWarning:

A value is trying to be set on a copy of a slice from a DataFrame.

Try using .loc[row_indexer,col_indexer] = value instead

See the caveats in the documentation: https://pandas.pydata.org/pandas-docs/stable/user_guide/indexing.html#returning-a-view-versus-a-copy| Month | #Passengers | Log_Passengers | forecast_log | forecast_passengers | |

|---|---|---|---|---|---|

| 132 | 1960-01-01 | 417 | 6.033086 | 6.053819 | 425.735873 |

| 133 | 1960-02-01 | 391 | 5.968708 | 6.171650 | 478.975744 |

| 134 | 1960-03-01 | 419 | 6.037871 | 6.199400 | 492.453690 |

| 135 | 1960-04-01 | 461 | 6.133398 | 6.232725 | 509.141110 |

| 136 | 1960-05-01 | 472 | 6.156979 | 6.368919 | 583.426973 |

| 137 | 1960-06-01 | 535 | 6.282267 | 6.507530 | 670.168960 |

| 138 | 1960-07-01 | 622 | 6.432940 | 6.503117 | 667.218211 |

| 139 | 1960-08-01 | 606 | 6.406880 | 6.324834 | 558.265074 |

| 140 | 1960-09-01 | 508 | 6.230481 | 6.209196 | 497.301356 |

| 141 | 1960-10-01 | 461 | 6.133398 | 6.063624 | 429.930518 |

| 142 | 1960-11-01 | 390 | 5.966147 | 6.168173 | 477.313188 |

| 143 | 1960-12-01 | 432 | 6.068426 | 6.206753 | 496.087694 |

Compute MSE

from sklearn.metrics import mean_squared_error

mse = mean_squared_error(test_data['#Passengers'], test_data['forecast_passengers'])

print(f'Mean Squared Error (MSE): {mse}')Mean Squared Error (MSE): 5279.13204916217